Disclosure: All links to products and services mentioned on FinanciallyFree.eu are affiliate links. If you go through them to sign up for a service I will earn a commission. Sometimes you will receive a bonus too.

Funds added

In March I added more funds to my Twino account, doubling my investment on the site. Twino is probably my favorite peer-to-peer investing platform so far, mainly because of these 4 factors:

- Competitive interest rate.

- There are no fees for investors.

- The secondary market is very liquid.

- Most importantly: The numbers are always correct.

Now, what do I mean by the last bullet? Wouldn’t companies that offer financial services always have a well driven engine that can be trusted? In reality, that is not always the case. However, the Twino engine that runs all the numbers, to make sure you are paid the correct amount on the right time, works flawlessly.

Trust is essential for investors

Twino is like a trustworthy financial supermarket where you shop all the loans you need. When you pay, you know you don’t have to double check the receipt. You get what you expect and the price is always correct. This is essential to building trust between the company and investors.

On Bondora I keep seeing small things that makes me wonder if I can trust their back-end system. DCA fees vary a lot. Sometimes more than 50% are deducted from a repayment. Other times I’m not charged anything for their services. I asked Bondora if they could give a clear explanation on how the collection process works, which they did, but it wasn’t clear at all.

The Mintos engine is very stable, just like Twino. The numbers are always correct and on time. The only disadvantage with Mintos is the 1% fee on secondary market transactions. The interest rate is about 12% on Twino and Mintos at the moment. If it wasn’t because of the 1% fee I would be equally satisfied with the two. If you are looking to start or expand your P2P lending adventure, I can recommend both of them.

Investing for my children

I use Mintos for my children’s savings account, they are not allowed to have an account of their own until they are 18 years old. Who invented a rule like this by the way? I expect the law was created to protect children from fraud but I think it should be possible to create an investment account in their name if their parents authorizes. The products and services offered by the public banks are, to put it mildly, not interesting. Thus, real investing is necessary if I want to build wealth for my kids.

Returns in April

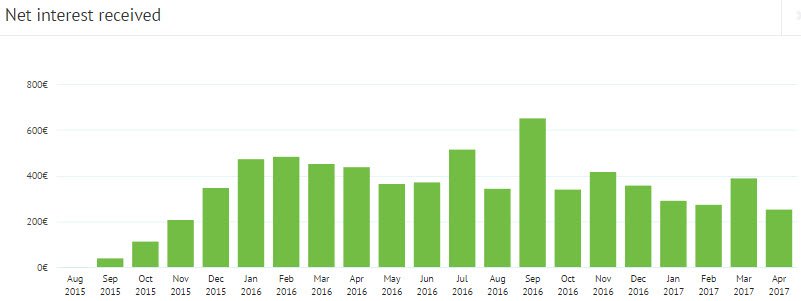

Net interest received for Bondora continues the downward trend. I can’t say that I’m overly satisfied with the progress lately. I’m reinvesting all repayments, both principal and interest. Eventually I would expect the Net Interest received to start rising eventually. I’m still waiting for the turning point…

Bondora returned 253,83€, (-136,73€ less than last month).

Twino returned 98,41€, (+45,74€ more than last month).

(new funds added)

Mintos returned 11,36€, (+0,07€ more than last month).

This gives me a total of 363,60€, (-90,92€ less than last month)

That equals 12,12% of my first goal, (-3,03% less than last month)

New initiatives

A few weeks ago I started looking into Swaper. After doing a good amount of research I decided to create an account and I just made my first deposit. I expect the money to arrive within a few days. I’m really looking forward to testing out their platform.

Swaper offers a fixed 12% interest rate and all their loans come with a BuyBack guarantee similar to Twino and Mintos. On top of that, “loyal customers” get +2% interest with Swaper, upping the game to a healthy 14% return on investments. “Loyal customers” is quite a diffuse term but, as I understand it, you can become a loyal costumer by providing feedback and sharing your experience with the Swaper development team. Apparently, investing more than 5.000€ should also give you the coveted title.

Remember to subscribe to my blog, to be informed about my Swaper experience. I will update you on the sign-up process and give an honest review already next month.

Comments are closed.